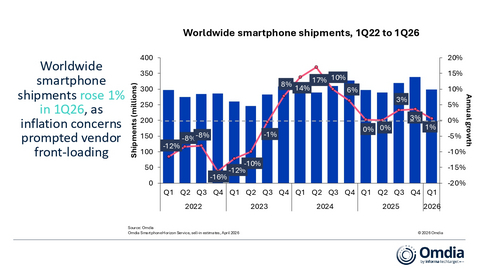

The global smartphone market shipped 298.5 million units in 1Q 2026, growing 1% year-on-year (YoY), according to Omdia. The quarter was shaped by two opposing forces. Vendor-led front-loading – as Samsung, Apple, and others accelerated sell-in ahead of expected inflation in memory and component costs – supported momentum and contributed to performance exceeding initial industry expectations. However, macroeconomic headwinds continued to weigh on end-consumer demand. Persistent inflation has compressed household discretionary budgets, creating a widening gap between channel sell-in and underlying sell-out. This imbalance is expected to lead to a more pronounced correction in 2Q 2026 and the second half of 2026.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20260429020190/en/

Worldwide smartphone shipments, 1Q22 to 1Q26

Vendor Highlights

Against industry expectations, Samsung retained its position as the world’s leading vendor, shipping 65.4 million units (+8% YoY). The result reflects resilience across both ends of its portfolio: entry-level A-series volume anchored emerging market shipments, while strong demand for the Galaxy S26 series drove premium growth.

Apple shipped 60.4 million units, up 10% YoY. The iPhone 17 series remained the primary growth driver, with the newly launched iPhone 17e delivering a particularly strong debut in telco-driven markets such as the EU and Japan. The iPhone 17 Pro and Pro Max outperformed their predecessors at launch, with Mainland China recording an especially strong result at +42% YoY.

Xiaomi shipped 33.8 million units, down 19% YoY, marking the steepest decline among the top five vendors. With more than half of Xiaomi’s shipments concentrated in the sub-$200 segment, the brand remains disproportionately exposed to memory cost inflation, which has compressed margins and weighed on volumes in its core price tier.

OPPO (including realme and OnePlus) ranked fourth with 30.7 million units, down 6% YoY, followed by vivo in fifth place with 21.3 million units, down 7% YoY. Both vendors recorded single-digit declines consistent with softer Q1 sell-through, following accelerated entry-level channel fill in Q4 2025.

Outside the top five, HONOR was the fastest-growing vendor in the top 10 with 19.2 million units shipped, up 19% YoY. Growth was driven by strong international momentum, as HONOR more than doubled its shipment volume YoY in the Middle East and Africa. In its domestic Mainland China market, HONOR declined amid intensifying competitive pressures.

Market Dynamics: Front-Loading, Inflation, and the Road Ahead

The Q1 2026 outcome reflects a market in the early stages of a supply-side disruption cycle, driven by sustained increases in memory, storage, and processing component costs. Omdia characterizes the current environment as the growth phase of a three-stage cycle, where continuous price increases incentivize vendors and channel partners to pull forward orders to mitigate future cost exposure.

- Front-loading effects: Vendors accelerated sell-in ahead of further anticipated cost increases, supporting headline shipment growth but creating an inventory overhang. Channel partners also built excess stock to hedge against rising end-prices, amplifying the pull-forward effect.

- Consumer demand divergence: While sell-in was elevated, end-demand remained more measured. Persistent inflation in essential categories compressed discretionary spending, extending replacement cycles and increasing consumer selectivity, particularly in mid-to-premium segments.

- Pricing pressure on entry segments: Vendors have begun passing through cost increases, particularly in entry-level models where margin buffers are limited. This has had a more pronounced impact in emerging markets, where price sensitivity is higher, further constraining demand and exacerbating the divergence between sell-in and underlying consumption.

“The Q1 2026 performance reflects a market where supply-side dynamics have temporarily distorted underlying demand signals. Front-loading activity across both vendors and the channel lifted shipments in the near term, but this has created an inventory overhang that will weigh on subsequent quarters as demand normalizes,” said Omdia Research Manager Le Xuan Chiew.

Market Outlook

The market is expected to transition from a period of front-loaded expansion into a more prolonged phase of adjustment, as elevated channel inventory is absorbed against a weakening demand backdrop. While near-term inventory normalization is anticipated from 2Q 2026, the recovery trajectory is likely to be uneven and more subdued than previously expected.

Inflationary pressures are expected to have a more pronounced and lagged impact on consumer demand in the second half of the year, as the cumulative effect on real incomes and discretionary spending becomes fully visible. This is likely to further extend replacement cycles and weigh on demand, particularly in mid-to-premium segments.

In this environment, vendor priorities will shift toward tightening sell-in discipline, managing inventory risk, and protecting margins, with volume growth remaining constrained. As a result, market performance in H2 2026 is expected to face downside risk, with sell-in increasingly aligned to cautious demand expectations rather than channel expansion.

“The smartphone market has entered a period that will be defined by significant disruption and structural change. Supply-side pressures, particularly across DRAM and storage, have intensified over the past nine months and will remain a critical factor shaping market dynamics over at least the next two years,” said Runar Bjørhovde, Principal Analyst at Omdia.

|

Global smartphone shipments and annual growth |

|||||

|

Vendor |

1Q26 |

1Q25 |

Annual Growth |

||

|

Shipment |

Market |

Shipment |

Market |

||

|

Samsung |

65.4 |

22% |

60.5 |

20% |

+8% |

|

Apple |

60.4 |

20% |

55.0 |

19% |

+10% |

|

Xiaomi |

33.8 |

11% |

41.8 |

14% |

-19% |

|

OPPO |

30.7 |

10% |

32.8 |

11% |

-6% |

|

vivo |

21.3 |

7% |

22.9 |

8% |

-7% |

|

Others |

86.8 |

29% |

83.9 |

28% |

+3% |

|

Total |

298.5 |

100% |

296.9 |

100% |

+1% |

|

Notes: OPPO includes OnePlus and realme. Xiaomi includes sub-brands Redmi and POCO. Percentages may not add up to 100% due to rounding. |

|||||

|

Source: Omdia |

© 2026 Omdia |

||||

About Omdia

Omdia, part of TechTarget, Inc. d/b/a Informa TechTarget (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets grounded in real conversations with industry leaders and hundreds of thousands of data points, make our market intelligence our clients’ strategic advantage. From R&D to ROI, we identify the greatest opportunities and move the industry forward.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260429020190/en/

Media gallery